At risk of sounding older than where I’m actually at, the 6% I’m talking about was in my younger days in my early 20s with a goal to see how far I can go to maximize muscle mass and prove some folks who claimed I was a “hardgainer” wrong for admittedly petty related reasons as well as maximizing bone density - which did work - my bone density is 99 percentile age-matched. I figured why not give it a shot for body fat percentage at typical bodybuilding competition levels of ~4-6% just for kicks (I didn’t compete in any actual competitions although I know a few old buds who did).

I still think it was likely a bad idea to go down to 6% personally, even at a younger age. I’m content with staying around 10-12% to be frank and it’s not particularly difficult currently but likely in the future it could be increasingly difficult.

Trading options for people is generally playing with fire - many burn out in 1-2 economic cycles so an outsized return in a year is almost certainly meaningless. Small amounts for hedging if you know how is generally a legitimate use, but very few retail investors are actually using options for this purpose. Almost always it’s just another gambler without an edge because pretty much any derivative trading is really, really hard to win in the long run.

Last year I made large returns without leverage, so what? Short-term returns are usually not meaningful, especially without repeatedly getting the exact rationale correct in advance - unless you’re going with technical analysis (which I do not use at all) and I don’t count that as meaningful in any stock analysis (as opposed to commodities which is a different story) but we can agree to disagree if you’re a TA guy.

Although I can’t speak for whether you’re some superstar or not, just asking the average retail trader about the very basics - the limitations on Black-Scholes or how they would price derivatives to gain a real edge is going to get some scratching heads. Often you’ll quickly rule out any real information advantage or edge from there and it’s just another average retail investor. But you are quite welcome to describe your options edge, as I’m quite familiar to an extent with pricing options and various forms of arbitrage in options.

Frankly, I don’t even trust most “pros”. Any guy from top 50 can make it one or another in the financial sector and claim they are a pro but have no real edge. Not to mention, the CFA is not particularly useful (I can pass level I and probably further anytime with the current financial knowledge I have, but it’s not particularly meaningful). I’m not even trying to brag in any form at all - talk to some top IB folks and some folks that actually run a non garage sized hedge fund it’ll become obvious what’s considered bragging or not. They’d probably laugh pretty hard at most retail investors only happily talking about their high 1-year return in isolation, so I really suggest you bring up something actually more meaningful.

In addition, if it’s easy for you, I sincerely suggest you (1) start managing money with audited returns (2) use a trade journal to document the exact rationale in specific terms for each trade, preferably with some indication of how you evaluate confidence levels of each trade. When you beat the markets with 2 economic cycles without getting blown away with a large loss, please do consider reserving a spot for me. I’ll even consider a little more than 1 economic cycle if the quality of your trading journal is high and timestamps are auditable. Not trying to be facetious.

I also guarantee if you keep beating biotech hedge funds in this fashion with your biotech stock investments (or really any sector or investment) - over time you will be very rich - in all seriousness. Hence if you can really do this consistently and don’t enjoy your current job or financial situation - I suggest you spend a disproportionate amount of time and effort on this and getting even a minimal amount of auditable documentation right.

Corporate bonds aren’t necessarily “safe” in the first place. I suppose Treasuries aren’t technically zero risk but the probability of default in the short term is essentially considered to be zero (or perhaps we will have larger problems than portfolio returns), as opposed to the corporate bonds you’re referring to which have a significant probability of default. In a significant recession, it’s more likely such bonds in the middle are hit hard closer relative to the junk bonds rather than closer to Treasuries. Seems to be zero edge so far.

I’ll also add that the public bond market is generally even more efficient overall and you’re playing against some really hardcore folks in bonds, particularly when it comes to “investment grade”. I’m not sure where you derived your assumption of safety. If your experience was only in the options dept, why play public corporate bond markets? And if you are confident enough - why not just bet on the Fed rates directly and size it based on the probability or simply buy long duration zero coupon Treasuries? You’re adding a lot more extra variables for yourself to evaluate risk on - it doesn’t seem to make sense at all for a one-man shop and I seriously doubt some informational advantage in the bond markets when you’re adding so many extra dimensions here. The human mind is less likely to derive enough research focus to beat the teams you’re up against doing this full-time with such a diluted approach.

Selling puts can be great until it isn’t even for those who have experience. There isn’t any specific you mentioned that would support the assumption that is it “safe” or even close to “safe” when we use risk adjusted returns. The 98% calculated doesn’t really matter. It’s kind of like how dumb using 95% or 99% VaR is for banks to appease regulators - it’s just done to make them feel better with no actual real meaning. Let me give an example - the same guys who said Lehman was “safe” said there was a ~1 in 10,000,000 chance of MBS default (not joking - that’s literally what a family friend said who is high up in the IB world). It looks “safe” until it isn’t and there are real tail risks here. As you are probably aware, tail risks tend to be higher than what normal distribution would predict. In fact, there are hedge funds with a lot more resources and research capabilities literally betting on far out-of-the-money puts that put sellers assume are “safe” to sell due to low probability of failure - until the hedge funds make off with 4-digit returns.

While there is a possibility of measured selling of say long-term puts as a strategy (since that’s partly where Black Scholes limitations lie with possible miscalculations by counterparties, just as an example that you probably are aware of), I don’t see a real edge here so far. And it’s got nothing to do with fundamental analysis regarding the accuracy in evaluating the probability of success in a clinical trial to appropriately size a position that I’ve previously mentioned.

While I’m not concluding it’s a horrible strategy - I just don’t see an edge here. Beating the SPY isn’t necessarily an accurate higher risk-adjusted return deal with the consideration that failure would lead to the leverage you are employing still potentially blowing up as a real deep downside risk. And if you are margin borrowing for those corporate bonds (hard to tell and is unclear but I presume possibly not) - can get you in a lot of trouble as you know.

There are just better ways to get high enough risk-adjusted returns. As an example, if you have an accurate probability assessment on longevity for older adults - one can already beat the insurance companies with fixed single premium insurance annuities (the annuities that are not advertised) that can be well above historical average SPY returns with truly “safe” near zero risk when under a state guaranty fund limit. There are also plenty of low-risk arbitrage situations or fringe inefficiencies that can fit this criterion and do not necessarily require leverage.

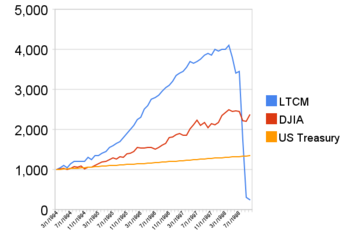

I suppose you’re familiar with the LTCM debacle with MIT and Harvard PhD professors? While I hope this does not happen to your portfolio, it illustrates the dangers involved even among those with decades of experience and plenty of decorations.

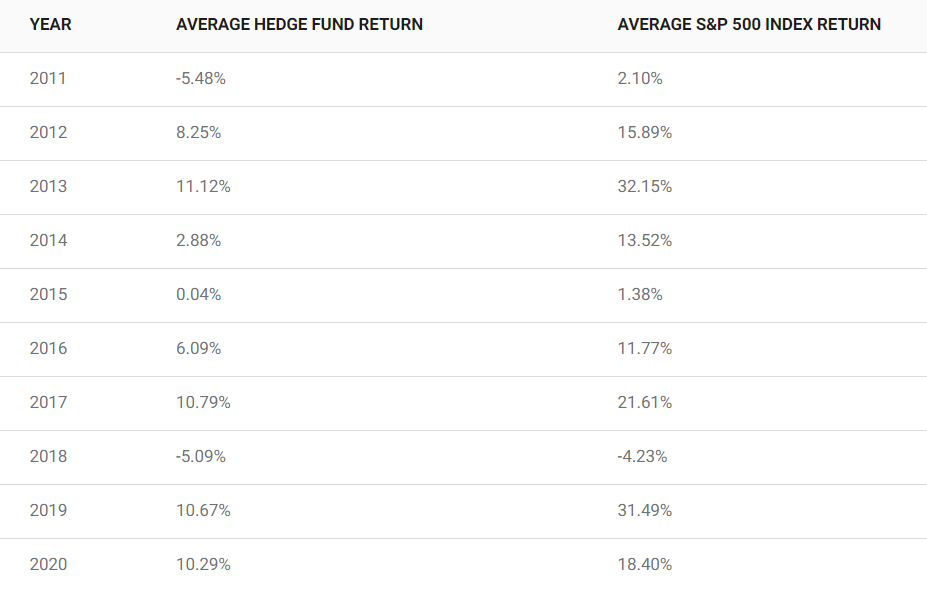

That data is not reflective of all hedge funds - many aren’t in that data. So one actually can’t say that’s the true average let alone biotech hedge funds, but okay - hedge funds can have an unclear definition in the first place.

My original comment was about beating the team of PhDs in biotech hedge funds that one is up against on the other side, particularly when it comes to biotech stocks, with the implication of fundamental analysis to determine probabilities in clinical trial success rates. So when you claimed in your reply it’s easy to make lots of money with the implication on biotech stocks, I assumed you were replying to that specifically rather than an unrelated general statement.

But either way it’s actually not “easy” as you claim and that’s reflected in the risks you’re taking which is more of “selling insurance” using extremely risky leverage with possibly catastrophic risks on complex derivatives, at least in part using highly questionable technical analysis. That’s why I think it’s pretty fair to say probably no real edge. It’s more likely akin to the classic metaphor “picking up pennies in front of a steamroller” - seems easy until it isn’t. I’m sure you realize the risks to at least some extent as you mentioned part of the risk and have some experience but any way you slice it, “safe” is an overstatement. The same goes for those higher-yielding end of investment-grade corporate bonds with what appears to be macroeconomic gambling on the future trajectory of Fed rates, which is also pretty hard to gain an edge as a one-man shop and the rationale is even more questionable when you also claim it’s “safe”, but it seems you’re at least somewhat aware of the even higher efficiency of those markets. I’m even more confident of an even higher likelihood there is no edge on the bond side.

One can certainly be as happy as one wants with your investment choices, but it’s largely irrelevant to the apparent problems with the methodology. I’d suggest avoiding the overstatement of claimed “safe” returns.

I sold my first tech business (created in 1983) in 2019. That business provided transaction handling services to brokers. Over the years I saw plenty of people go bankrupt from writing/selling options. Its picking up pennies in front of a steam roller.

I have done reasonably well out of investments, but I am a long term value investor.

For what it’s worth, I’ll add fundamental analysis merely puts odds on one’s side and I don’t really subscribe to a “typical value investor” viewpoint although whatever works for y’all.

In case anyone is interested in a slightly different perspective - my view is the practical approach would be searching for fringe inefficiencies or arbitrage opportunities that may yield very high returns for low risk when portfolio < 10M - because there is only so much focus one person can put in where it will move the needle - a majority of mine is just not in finance, so it better be large enough returns to move the needle.

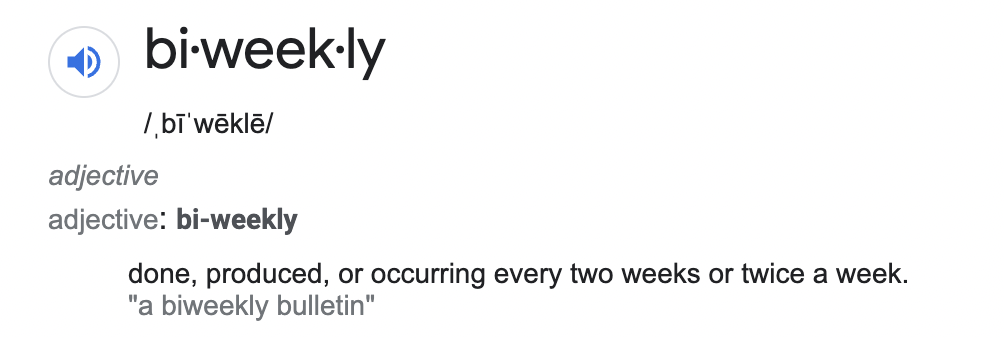

I’m pretty sure that when Bryan Johnson says on his website that his dosing is 13mg rapamycin bi-weekly, he means once every two weeks… not twice a week. the “bi-weekly” term is frequently misinterpreted and confusing.

He’s getting press, which he seems to be happy about, but the vast majority is negative. He ends up coming off as an obsessive millionaire wasting money on a fantasy more than someone following the cutting edge of actual science.

Matt Kaeberlien’s dogs are going to be a much better poster child for rapamycin than Bryan Johnson. Everyone wants more time with their dogs, who are pure of heart and not obsessive about anything except getting up each day to be a dog to the fullest of their abilities. And if rapamycin helps dogs, it will be seen as a universally positive thing. Whereas any gains that Bryan Johnson gets from the “2 million dollar regimen” in an era where people can’t afford their prescriptions in America will be seen as a case of wealth inequality taken to the extreme and agitate people to break out the guillotines.

Dogs are way more sympathetic than tech millionaires.